The recession everyone hoped would end quickly has now lasted for two years, at first causing fear and concern that now has turned to grit and determination to hold on until better times. While no one sees the current market as ready to take off, major firms are beginning to think the market may soon hit bottom and slowly begin to pull itself back from the brink in 2011.

The ENR Construction Industry Confidence Index (CICI) for the second quarter of 2010 shows 555 executives from construction and design firms believe that, while the market continues to flounder, next year it will be on the rise. The index for the second quarter of 2010 rose dramatically to 41 on a scale of 100 from the first quarter’s 34, and it showed a 10-point rise over the fourth quarter of 2009.

The CICI measures industry sentiment regarding the current market and beliefs about where it will be in three to six months and in the next 12- to 18-month period. An index of 50 would mean a stable market. The CICI is based on responses to surveys sent to more than 2,000 U.S. firms on ENR’s lists of leading contractors, subcontractors and design firms. The current index is based on a survey conducted over a two-week period earlier this month.

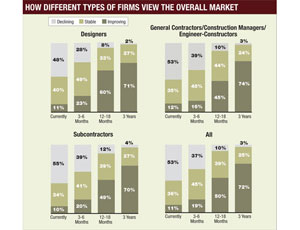

While 53% of all respondents say the market still is in decline, this percentage is an improvement over the first quarter, when 68% saw a declining market. Further, only 37% believed the market would continue to decline over the next three to six months, compared to 45% in the first quarter. As in past surveys, designers continue to be more optimistic about a turnaround in the short term than general contractors or subcontractors (see chart, p. 53).

Survey respondents showed increased confidence in almost all market sectors measured by the survey. Applying the CICI rating formula, only the petroleum market, rocked by economic and regulatory uncertainties in the wake of the BP oil spill in the Gulf of Mexico, saw a significant decline—from 51 on a scale of 100 in the first quarter to 44. The only other market sector to lose ground was transportation, going from 55 to 54.

Health care was the market about which survey participants were most confident, earning a rating of 65. The only other buildings market in positive territory was higher education, at 52.

While most markets in the buildings sector gained over the past quarter, respondents continued to believe the recovery in the sector still is a long way off. The only big improvement in attitudes in the buildings sector was multi-unit residential, which rose from a 31 rating to 39.

Infrastructure markets continue to be seen as the healthiest, with power (64), hazardous waste (63) and water, sewer and wastewater (62) the strongest.

CFMA Sees Uptick

The uptick in confidence is paralleled by the most recent CONFINDEX survey, about to be released by the Construction Financial Management Association, Princeton, N.J. CFMA polls 200 chief financial officers from general contractors, subcontractors, and heavy and civil construction firms. “Our CONFINDEX went from 101 to 108 for the second quarter of 2010,” says Mike Verbanic, CFMA’s director of marketing.

CFMA’s index is based on a scale of 200, with 100 being a stable market. Verbanic notes the CFOs surveyed found general business conditions, including backlog and availability of bank credit, much better than a year ago. “There are no signs of euphoria in the survey, but more of a sense that market conditions are slowly improving,” he says.

As for market prospects, the CFMA survey rating dropped slightly from 129 on a scale of 200 in the first quarter to 127 in this quarter, notes Brian Summers, CFMA’s chief operating officer. “Attitudes about the market are still not great, but they are a far cry from where they were in the fourth quarter of 2008, when the CONFINDEX was 79,” he says.

Another indicator showing positive signs is the Architecture Billings Index from Washington, D.C.-based American Institute of Architects. The ABI for April, released on May 21, was 48.4 on a scale of 100, the highest it has been since January 2008. AIA chief economist Kermit Baker cautions that any score below 50 means a decline in billings, but says this decline has slowed considerably.

The ENR CICI survey also asked about the ease of obtaining project financing. While the responses generally were negative, they were not as grim as in the first quarter. In this quarter, 39.3% said obtaining project financing was tougher than six months ago, which is a marked improvement from last quarter when 50.7% said financing was tougher to obtain. Also, 13.0% said project financing was getting easier in this quarter, compared to 7.2% in the last quarter.

While the market remains in the doldrums, many industry firms worry about inflationary pressures once it turns around. Thus, the CICI survey asked if firms had seen any upward price pressure. Of the 330 respondents that answered this question, about half said they had seen little or no upward pressure on prices.

On the other hand, 112 survey participants said they had seen a rise in steel prices, which was more than for any other commodity or material. “Yes, steel has been increasing for the past 60 days,” says one general contractor.

There have been price increases in several categories. Copper prices also are on the rise, according to 44 firms. Concrete and cement (38 firms), lumber (37) and drywall (28) were the most frequently mentioned categories.

Several mechanical contractors around the country mentioned a sudden spike in sheet-metal prices. Two mechanical contractors from different parts of the country said they have seen a 15% rise in sheet-metal prices within the past 90 days.

These increases have led to a level of concern. “Even though demand has not increased, copper is high, concrete is rising, and price increases in drywall are coming soon,” says one general contractor in the Southeast. “Yes, prices ... are edging up even without an apparent increase in demand,” adds another GC in the Southwest.

Post a comment to this article

Report Abusive Comment