Related Link:

ENR MidAtlantic 2023 Top Contractors

A recession loomed when ENR MidAtlantic published the 2022 Top Contractor ranking last August. One year later, the economy is chugging along despite the threatened downturn constantly nipping at the heels of the region’s contractors.

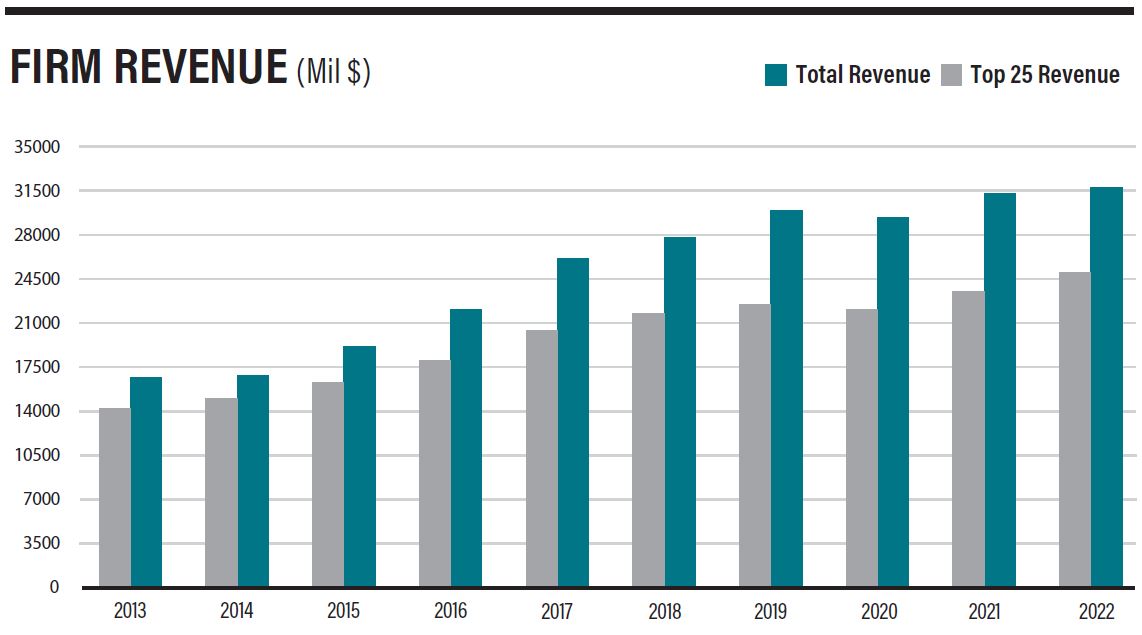

The 70 firms on this year’s list recorded $31.86 billion in regional revenue. That’s up 1.7% from last year’s ranking, when 76 firms reported $31.33 billion in MidAtlantic regional revenue in 2021.

But this year’s report also shows that the largest contractors in the region continue to post bigger revenue gains. Based on 2022 revenue billed in Delaware, Maryland, Pennsylvania, Virginia, West Virginia and the District of Columbia, this year’s top 10 firms collected a combined $17.92 billion in revenue, a 12.49% boost from the $15.93 billion reported by last year’s top 10 firms.

Moving Forward, Cautiously

No. 5-ranked DPR Construction contributed to that trend, recording $1.18 billion in revenue, up 10.28% from last year, when the firm was ranked No. 7 with $1.07 billion in revenue.

Camilo Garcia, business unit leader for the Reston, Va.-based firm’s D.C./Baltimore offices, notes that a “robust backlog of projects” is scheduled for construction during the next few years. “While new starts may slow down, we see it as a leveling off—adjusting to this new normal coming out of the pandemic,” Garcia says. “Companies and institutions are being cautious, but [they are] moving ahead with projects.”

Garcia says more technical projects will restart in the final quarter of the year “as capital will need to be deployed. The capital projects they paused several years ago are still needed, and they are starting to move forward.”

He notes a 7% increase in contract values for projects his firm is building compared with projects at the same time last year. Garcia says a “significant” number of projects valued at more than $100 million are “starting to activate.”

Building relationships with trade and supply-chain partners has become more important than ever, Garcia says, to ensure materials are available and to source alternatives when they are not.

“Construction teams evaluate risks to the project and develop contingency plans,” he says. “Our ever-forward approach to our business has taught us to be flexible and adapt while challenging the market to evolve and do things differently.”

The Big Three

The top three firms on this year’s list are also thriving. For the first time in the survey’s history, each of the three leading firms brought in more than $3 billion in revenue. Last year, only the No. 1 firm on the survey, The Whiting Turner Group, collected more than $3 billion, recording $3.21 billion.

This year, Whiting-Turner fell from the top slot on the ranking for the first time since 2018. The Baltimore-based juggernaut’s $3.27 billion in regional revenue on this year’s survey placed it behind HITT Contracting Inc. and Clark Construction Group.

HITT’s $3.39 billion in revenue this year advanced it one spot, to second place, thanks to a 53.39% revenue increase from the $2.21 billion it logged last year.

Last year, HITT’s revenue climbed more than 38% from the previous year’s $1.6 billion, which was a 7.75% decrease from the previous year.

Clark, which was No. 1 in 2018, returns to the top spot this year with $3.70 billion in regional revenue. Clark’s revenue this year represents a 28.92% increase from last year’s $2.87 billion, which was up 10.38% from approximately $2.6 billion the previous year.

Ryan McKenzie, group chief executive at Clark Construction, leads the firm’s Eastern group, which includes projects in the Baltimore metropolitan area and greater Richmond. McKenzie says Clark has successfully managed “historic supply chain bottlenecks and material shortages in recent years.”

He adds, “While we see lead times trend down, we continue to optimize our procurement and contracting strategies to ensure greater resilience and mitigate the risks of material-related disruptions on our projects.”

McKenzie also leads the development and delivery of Clark’s health care, life science, mission critical and industrial projects across the Washington, D.C., metropolitan area. He says health care, higher education, mission critical, sports, life sciences and water/wastewater “have seen strong growth in the MidAtlantic region.”

McKenzie says commercial projects, such as offices, have cooled during the past 18 months “due to clients’ desire to wait out interest rate fluctuations.”

Rebounding Health Care Market

The health care market represented $3.27 billion worth of work on this year’s survey, down 15.50% from the $3.87 billion in that sector on last year’s survey.

Labor and material shortages forced owners in the health care sector to put capital projects on hold and to defer maintenance during the last few years. But, Garcia says, “Health care systems are now cautiously moving projects forward and updating their facilities.”

Garcia also notes that the MidAtlantic receives the fourth-largest amount of National Institutes of Health funding compared with other regions in the country. That, in turn, is fueling growth in the area’s life sciences sector. “Navigating the unique requirements and demands from big pharma to start-ups for more flexible, innovative, mixed-used lab and manufacturing spaces that are move-in ready is in demand,” Garcia says.

He also says the CHIPS Act has created significant opportunities in the advanced manufacturing market. There will be “more than $160 billion of construction for new plants and 28,000 new American jobs—and that doesn’t take into account increased spending by other supporting industries,” such as housing and infrastructure near each semiconductor plant, Garcia says.

Post a comment to this article

Report Abusive Comment